From Third World to Utopia: Singapore could end poverty for our children forever, today

Mon Jan 18 2021tags: public draft economics exploration

Introduction

If the Singapore government earmarked $200,000 for each child at birth and let it grow until the child turned 18 before dispensing it, we could guarantee a basic income of ~$800 (inflation-adjusted!) every month in perpetuity without ever depleting the capital.

As the birth rate is 40,000 a year, guaranteeing such a basic income to all future children would cost the government 8 billion a year. Better yet, since the capital is never depleted, the capital from the first cohorts can be "recycled" for future cohorts once the first cohorts die out. The total cost is therefore bounded at $800 billion dollars (8 billion * 100 years lifespan).

I won't devote too much space here to defending a UBI; these arguments have been covered elsewhere. This essay aims to show that a UBI is actually well within our reach; I'll punt on the question on whether we'd want it to others. But if UBI really is as wonderful as its proponents say, and it is within our reach, we might just be one step from Eden.

The theory

Money makes money. If you put your money in the stock market or in bonds your money will always grow in the long run. So if you have a large enough sum of money you can withdraw a small enough sum of money such that the growth rate of your money exactly equals your withdrawal rate plus inflation. This means that that initial sum of money could theoretically last forever--ergo, a BI.

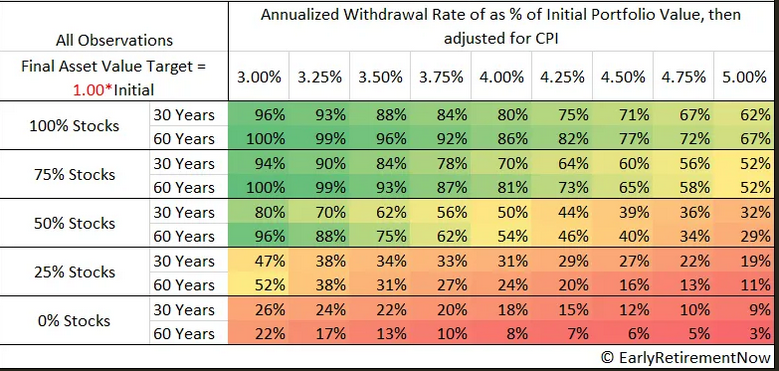

One glaring problem with this strategy is volatility: unfortunately, stonks don't always go up. However, we know that if you wait long enough stonks do always go up (in recorded history). And so the initial losses can be made back by future gains as long as your withdrawal rate is low enough. The good news is that pension funds and people who aim to retire early run these calculations all the time. Early Retirement Now find that over all 60 year time horizons a portfolio with 75--100% equities always manages capital preservation (if not growth). And in fact our government has it easier than this because sequence of returns risk is greatly reduced since the government is always both withdrawing (for older cohorts) and investing (for younger cohorts) at the same time.

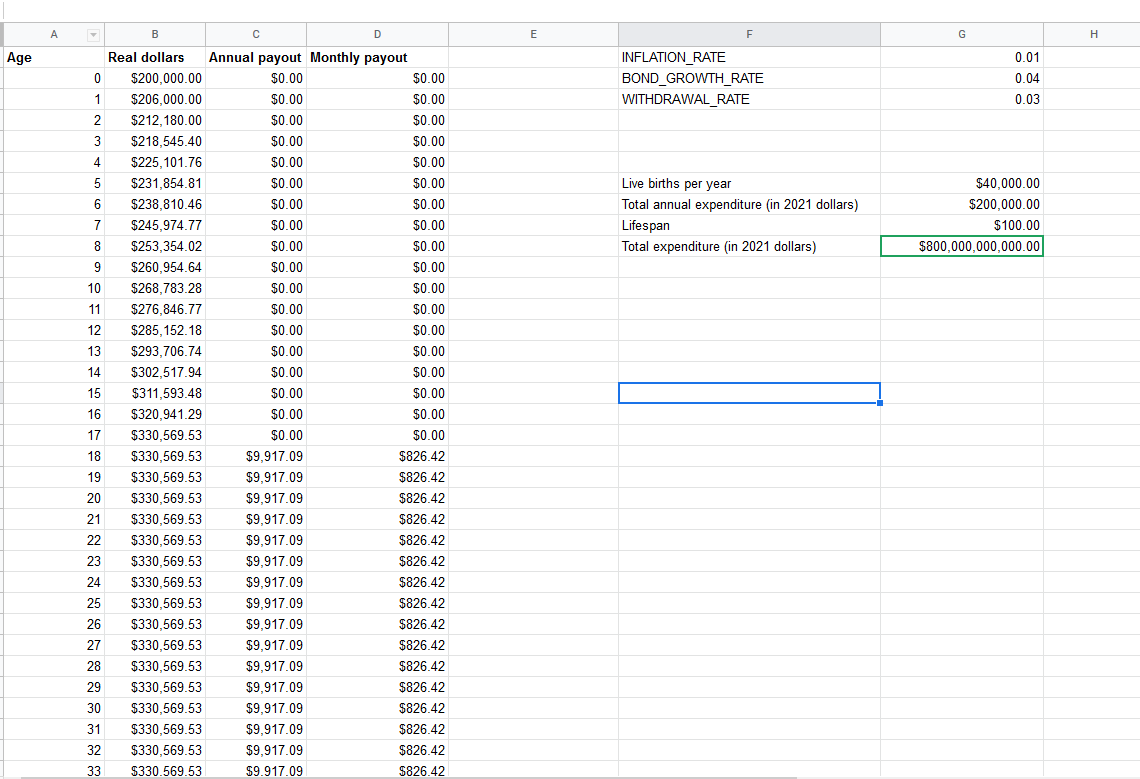

So, in detail: if the government constitutionally guaranteed a 3% real interest rate (similar to what it does for CPF) for 18 years, $200,000 at year 0 would become $330,569 in year 18 (after adjusting for inflation). This would allow a withdrawal of $9,917 a year, or $826 a month. And this capital would never be touched. On death, the capital would be clawed back by the government, ready to be endowed to the next person.

Can we afford it?

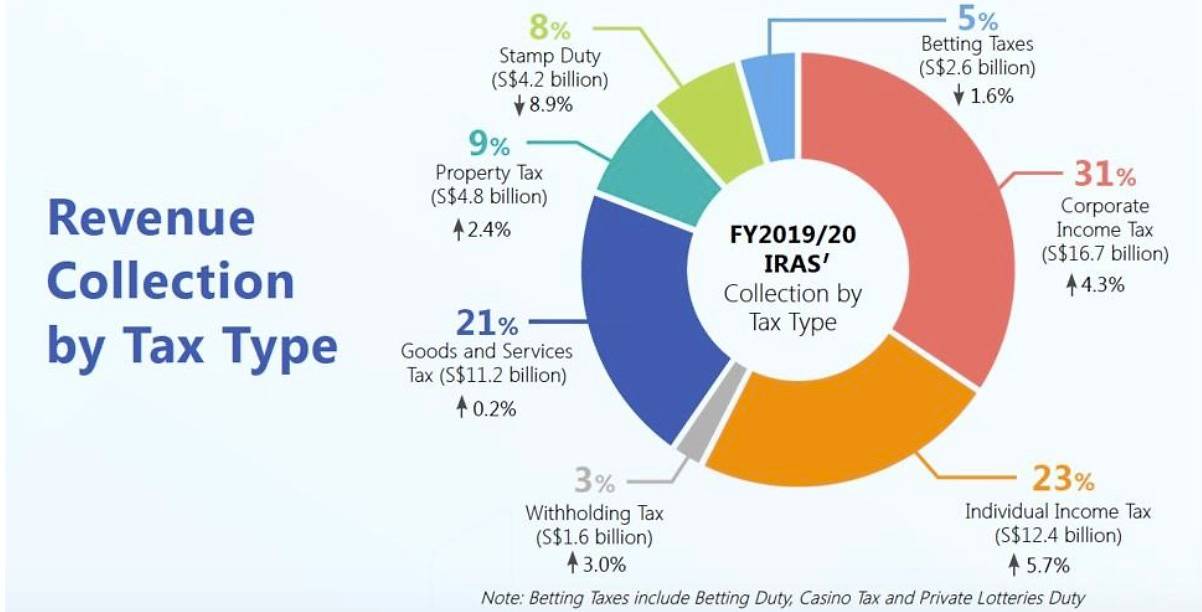

How much is 8 billion? It sounds like a lot, but it's not that much, really. Singapore collected 2.6 billion in betting taxes alone (wild! I wonder how much comes from Singapore Pools and how much the casinos). Singapore collected 11.2 billion in GST, 12.4 billion in income taxes, and 16.7 billion in corporate taxes.

And our net investment returns contribution (NIRC) from our reserves last year was 18.63 billion. This is half of our long-term expected real return.

The Net Investment Returns Contribution (NIRC) to the government budget consists of two parts: up to 50% of the Net Investment Returns (NIR) on the net assets invested by GIC, MAS and Temasek Holdings, and up to 50% of the Net Investment Income (NII) derived from Past Reserves from the remaining assets.

The government put in 6 billion to the GST Voucher Fund last year. As the GST Voucher Fund is a permanent one, the government is likely to continue contributing that amount to the fund.

I really like the idea of the GST Voucher Fund (it's kinda-sorta UBI-lite). But if 6 billion for the GST Voucher Fund sounds good, how does 8 billion for the Free Money For Life For Everyone Born After 2021 Forever Fund sound?

Why not a more targeted welfare programme?

We can and should certainly do more for the bottom 10-20% of Singaporeans.

But I think there are political reasons why this might be more popular.

TODO: To flesh out here.

Something about universality being more popular Give the example of the UK's NHS being popular with the rich even though they are certainly paying more than they would under a privatised healthcare system Another point: we have to have a dream; a dream that excites people and gets them on board. Targeted welfare doesn't sound like a dream; ending poverty for our children does.

Why give money to the unborn and not the people who desperately need it now?

Three reasons:

- The yet-unborn are going to have to bear a greater burden because of our shrinking population;

- We can't quite afford to give UBI to everyone;

- Parents spend a lot of time thinking, talking, and worrying about their children, so helping the children will help the parents.

TODO: To flesh out here.

Will a UBI not encourage indolence?

There's not enough research on UBI. But as far as the research shows, disincentives to work are minor.

But even if it did: what's wrong with indolence? Is our work-life balance today healthy? Should we have to put up with working 60-hour weeks and weekends? Don't we want our children be able to spend more time with their children? Isn't this something we should fight for?

A UBI isn't a panacea

I might have overpromised: it's not going to solve poverty. You'd still want comprehensive medical coverage (mandatory health insurance) for every citizen at the minimum.

But it'd go a long way: be it not having to be in arrears not worrying about not being able to make the rent of your rental flat, being able to afford the $500 co-pay (after MediSave deduction) of your cataract surgery...

What would it take to give every citizen a UBI?

35 billion annual payment forever, or 1.2 trillion set aside as a one-time payment. Our annual government revenue is 50b (with 18b NIRC), and we have maybe ~1 trillion as reserves, so we'd either need to double our reserves or devote all our reserves to UBI, which would not be financially or politically feasible.

The nice thing about this plan is that it's a "ramp up plan": it basically gives a small percentage of the population (those born in or after year X) a UBI every year. Eventually all people will be born in or after year X, and everyone will have a UBI.

Reference

Income for All Stanford BI Umbrella Review Measuring Poverty in Singapore